Cognizant: 7.5x FCF, margin expansion, activist sway. Nah, I still don't like it, says Mr. Market

Last week, CTSH 0.00%↑ was excluded from Nasdaq-100 index and fell to its lowest level since 2013. The company now has a 13% FCF yield, a 0.9 price-to-sales ratio, and guided margin expansion. This gap makes sense if we believe AI is about to destroy Cognizant’s business model. Should we believe it, though?

AI disruption risk

Cognizant is an IT consulting and outsourcing company. Both words sound like the primary victims of AI: it can analyze data, give you advice and write code. Why bother hiring a company that will likely just delegate the task to an LLM anyway?

To answer, we need to understand the scale and complexity of Cognizant’s contracts. In short: the clients are corporations, governments, universities, hospitals. Big organizations with legacy code, concerns about privacy and compliance, entrenched processes. They sign $100M checks for IT overhauls because it is a hard thing to do.

Vibe-coding another useless note-taking app is one thing. Replacing a system written in a programming language that was fancy in 1990 and launches from floppy disks is quite another. AI can speed up this process, but it still requires oversight, orchestration and eyeball testing.

AI could still be a headwind. It gives to the clients additional arguments for negotiating prices down. That’s the crux of the matter: who will reap the efficiency gains: outsourcing firms or clients? I think IT firms are better positioned. First, they’re just closer to AI and better understand it. Second, negotiating IT contracts is their core competence: they do it non-stop.

Of course, the situation might change if there is AGI around, but AGI will change everything in every industry. So for now I’ll stick to the current facts and trends shown in data.

Reverse-DCF: the market is pricing in big troubles

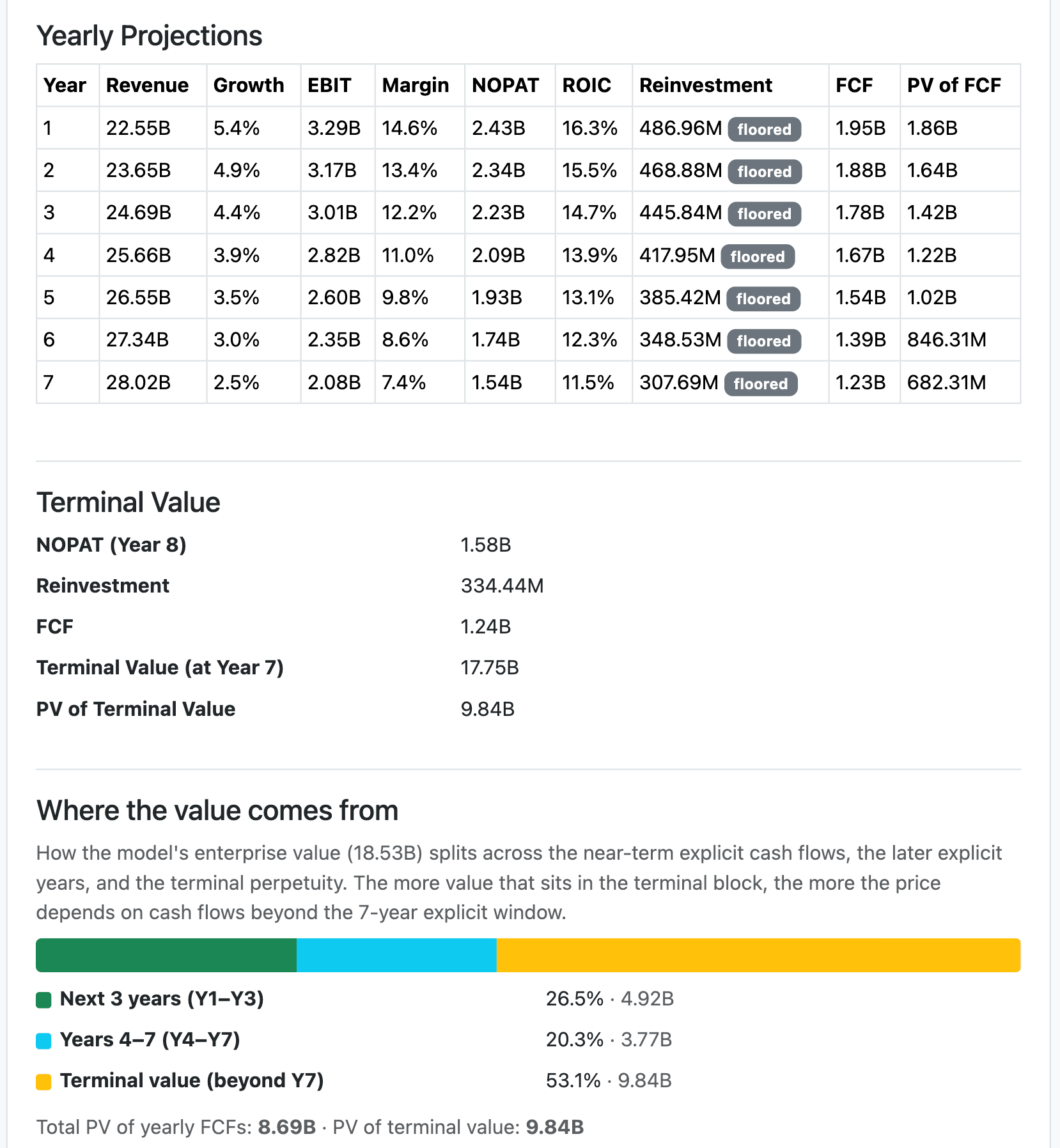

Let’s use expectations investing framework to understand what the price $40 implies1:

Let it sink in. This scenario shows:

Weak growth fading to 2.5%.

High CAPEX: enough to acquire something like Astreya2 every 18 months which (see the previous point) brings almost nothing.

Quick margin erosion: we have 16% - 16.2% guided and 15.8% TTM now; the model shows 7.4% at 7th year.

It looks like a real apocalypse, at least compared to current metrics. Margins around 7% were never present in the company’s history.

Current trajectory

Let’s take a look at the last earnings call.

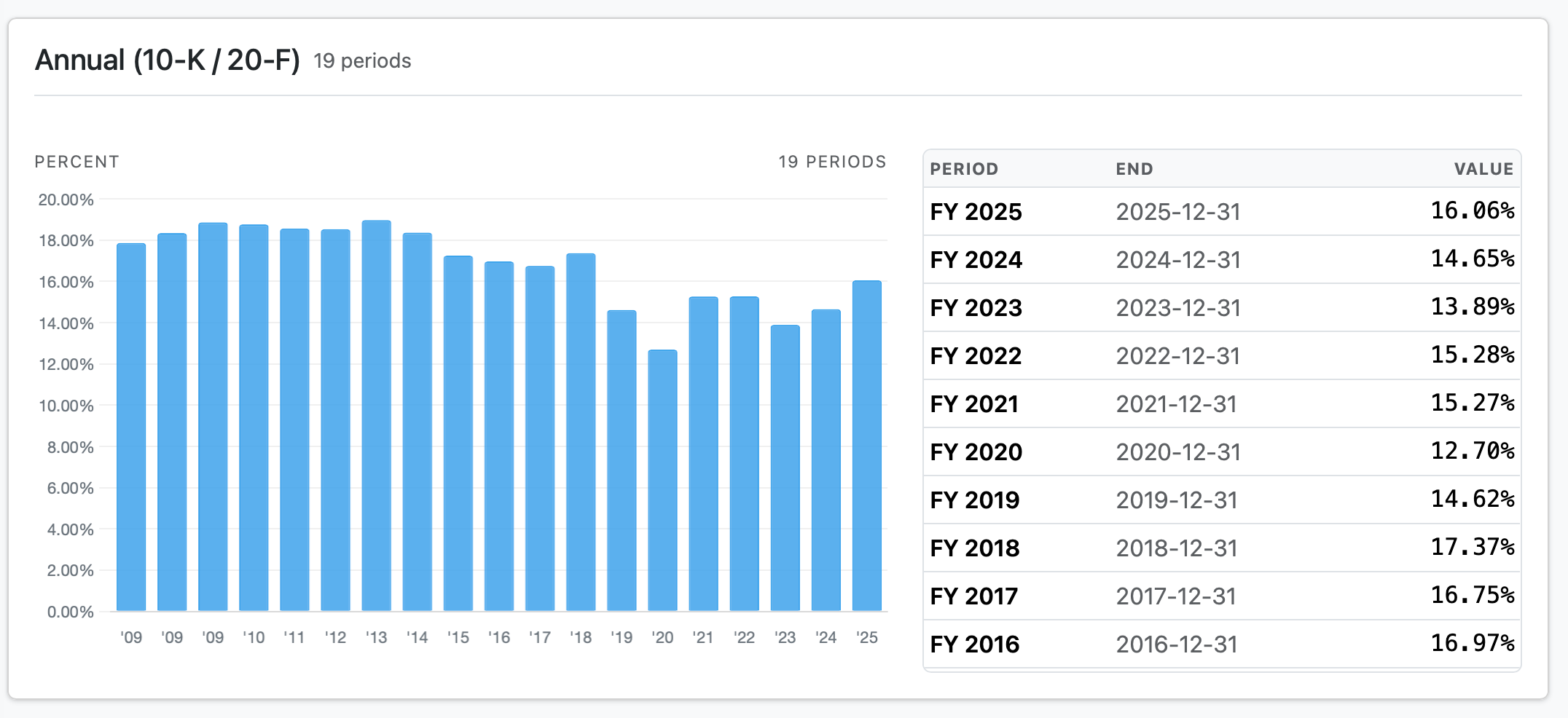

1. Margin is improving

Importantly, we continue to drive profitable growth as adjusted operating margin expanded year-over-year for the fifth straight quarter.

Even unadjusted, GAAP operating margin is clearly improving in the last three years:

For 2026, CTSH guided 20 to 40 basis points of margin expansion.

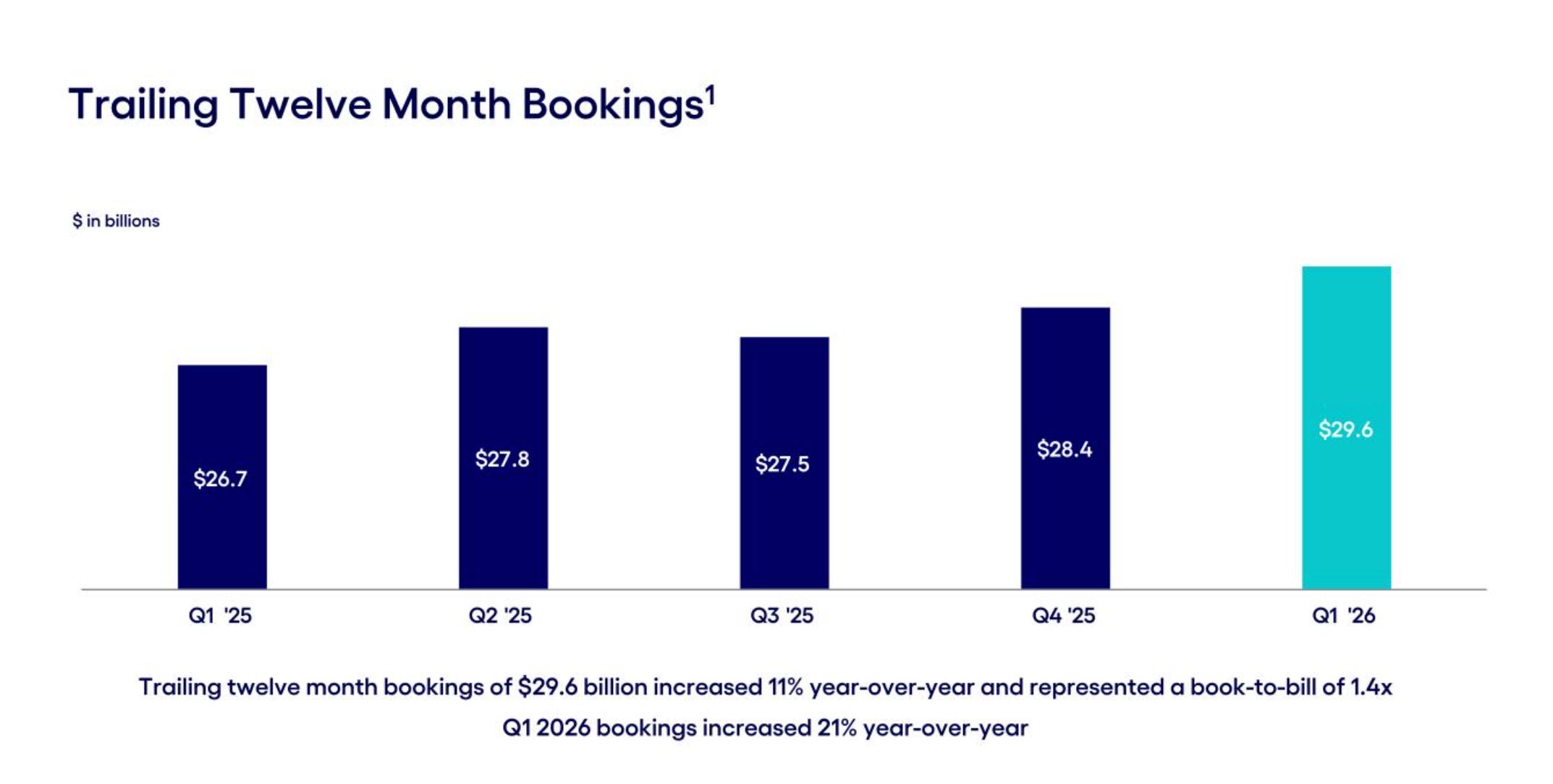

2. Bookings are growing

$29.6B is impressive. I am reluctant to cheer3, though. Bookings are tricky beasts. They aren’t auditable. They can be cancelled. They mix genuinely new deals with simple extensions.

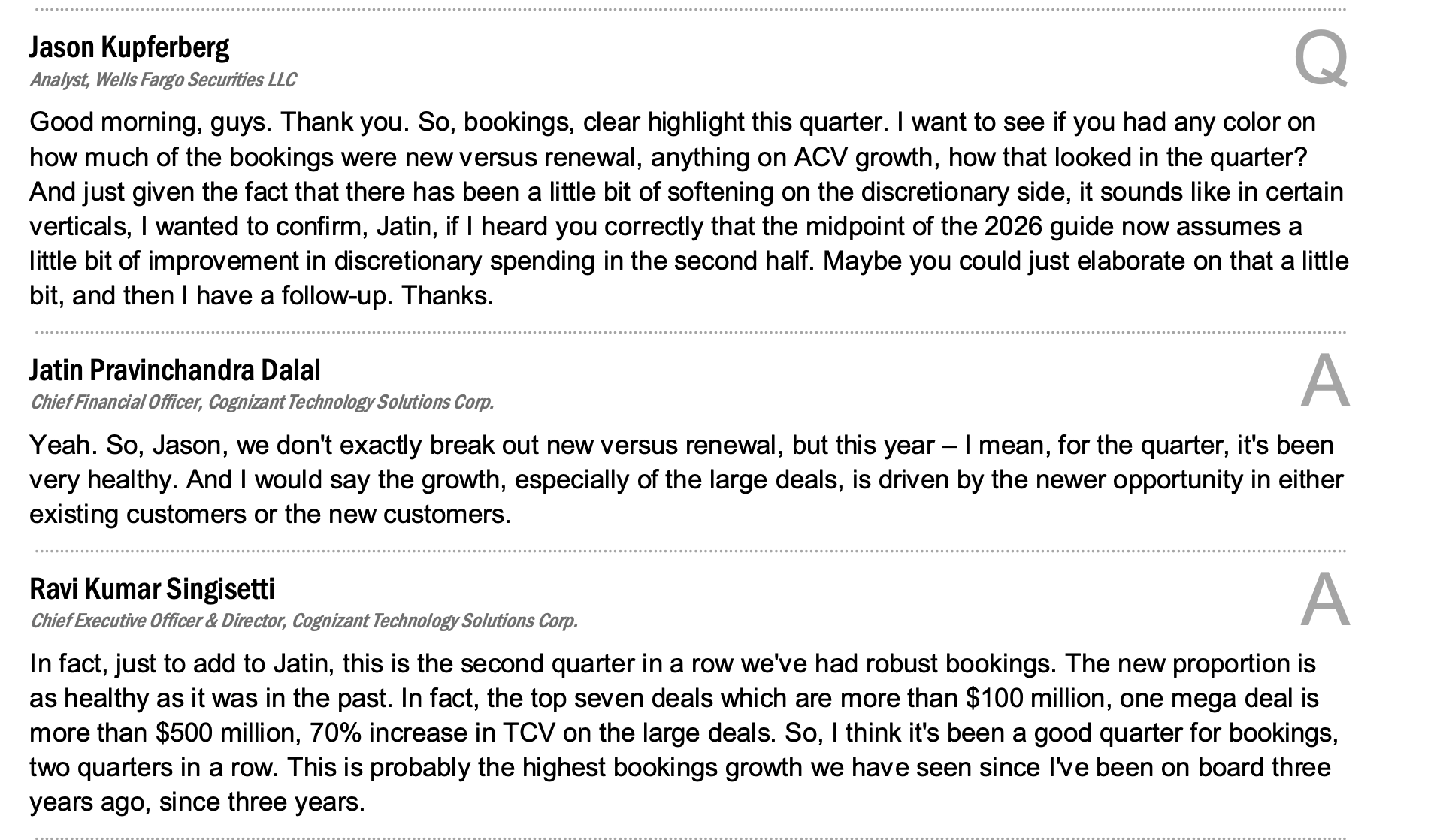

The very first analyst question was aimed exactly at this vague figure:

Management didn’t give a straight answer, but they shared an important detail anyway: “the new proportion is as healthy as it was in the past”. So if this 21% increase in bookings was just a manipulation of statistics, this framing would open the CEO to a lawsuit. It is reasonable to assume that Cognizant does indeed have real growth of bookings. A good sign. Even if we assume the worst — that the bookings were achieved with discounts and extending contracts, it still adds to the company’s stability. Stability in revenue is important as ever: it gives room to maneuver during the ongoing transformation and money to buy back shares at low valuation.

3. Selling, general and administrative expenses are flat

In Q1 2026 the SG&A is $791M. Exactly as it was a year ago, despite growing revenue. That’s a sign of improving efficiency and capital allocation discipline.

Management and activists

Last year, it became known that Mantle Ridge, an activist hedge fund with an impressive track record, quietly acquired a $1B stake in Cognizant.

Mantle Ridge is known for taking large board representation at their portfolio companies, often a majority, and replacing the CEO. None of that is happening here. This is a strong signal that Mantle Ridge likes the new CEO and is supportive of the actions that the board is taking. While we could not identify any direct relationships between Hilal and current board or senior management members, he is very well connected in many industries, and we would doubt there is more than one degree of separation between him and many of the key players here. Activists coming into underperforming stocks and taking action is generally a strong sign of potential future shareholder value. What may be an even stronger sign is an activist coming into a stock and not having to act.

CNBC, “How activist Mantle Ridge’s presence at Cognizant can help lift the company’s valuation”.

There is no clear data on the price of acquisition, the estimates land around $50-$60. Which, if we allow a bit of speculation, means the fund sits in a deepening red zone and under pressure of its own investors. So they’re unlikely to cut management any slack. CNBC article I quoted argues that the supportive stance is a good signal. I think being supportive and strongly financially motivated to succeed is even better.

Management compensation schemes are perfectly aligned with the activist profile. The CEO’s base salary is $1.3M, the whole package is around $20M, at least half of that is strictly performance-based. The management is strongly incentivized to deliver better margins and earnings per share.

Sentiment and repricing catalysts

Analyst recently cut price target for Cognizant; though even the lowest price target is $42, higher than the current price.

I am genuinely surprised that the stock is hardly ever discussed on Substack and FinX. These are the rare exceptions:

Cognizant increasingly emphasizes its position as an AI builder. Recent acquisition of hyperscaler-related Astreya strengthens the narrative. o if they continue to expand margins, execute buybacks, and deliver an EPS surprise, the sentiment can flip quickly; everyone would suddenly start reasoning that AI is actually a tailwind for efficient and modern IT outsourcing. The repricing would likely lead to reinclusion to Nasdaq-100 and mechanical buy pressure; possibly even euphoria and overvaluation.

Conclusion and my investment decision

I am not saying that Cognizant is a bargain. There are risks, as always. The demand might drop on rate hike worries. The competitor (Accenture) bookings softness is real and might signal industry-wide problems. Cognizant has recent acquisitions to integrate, which is not an easy task. Be aware of the risks, do your own research and and never buy just because some guy on Substack says he likes the stock.

Why do I like it? Let’s summarize. Given the pessimistic reverse-DCF, strong emphasis on shareholder returns through both buybacks and dividends, and recent improvement in margin and bookings, I decided to allocate up to 5% of my portfolio. I have not added to my initial position (entry at €34.97 ≈ $39.74) yet. I set several limit buy orders (a ladder below the current price). I think given the momentum, the price can drop further. I intend to review the position again just before the next earnings.

I will probably buy it in July anyway, if it won’t jump higher than $45. It’s not often a retail investor has an entry point 25% lower than an elite hedge fund.

This publication is for informational and educational purposes only. It is not investment advice, tax advice, or a recommendation to buy or sell any security. I am not a licensed financial advisor. Investing involves risks, including the possible loss of capital. Always do your own research or consult a professional before making financial decisions.

Here are the numbers I used in my model:

Shares: 473,869,469 (https://tools.theinvestlog.com/calculators/adjusted-shares/#CTSH).

TTM revenue: $21.406B (FY25 21.108 + Q1'26 5.413 − Q1'25 5.115, https://tools.theinvestlog.com/financials/CTSH/#concept=us-gaap%3ARevenues).

Total debt: 1092M (535M long-term + 33M short-term + 524M leases, https://tools.theinvestlog.com/financials/CTSH/)

Tax rate: 26% (the guidance).

Growth: starting with observed 5.8%, fade to 2.5% terminal (inside the guidance range).

Cash and short-term investments: 1517M (1504 cash and equivalents, 13M short-term investments, 10-Q)

TTM EBIT: $3.379B (3.389 + 0.843 − 0.853), https://tools.theinvestlog.com/financials/CTSH/#concept=us-gaap%3AOperatingIncomeLoss)

WACC: 9,5%. Cognizant is almost exclusively equity-funded. 5-year beta is around 0.8, which is misleading. The current market clearly treats CSTH not as a defensive asset, quite the opposite. So at least we should assume cost of equity on the market level: risk-free rate plus US ERP, which gives us: 4.47%+4.46%=8.93%. I think bumping it to 9.5% is completely reasonable, especially given the fact that many of the company’s operations are actually located in India which has higher ERP.

Stockholder's equity: 15068M (10-Q).

Reinvestment: floored as 20% of NOPAT.

Astreya is an IT services focused on AI infrastructure and data centers; among its clients there are 6 from Mag7. Cognizant recently acquired Asterya for $600M. I did not model the acquisition in the DCF because the effect is not shown in filings yet and it is hard to estimate it (Astreya is a private company). If we assume the deal was an absolute disaster and simply subtract 600M from the company’s cash, the picture doesn’t change much. To justify the current price the terminal margin would just be 0.4% higher.

You know, in FinX typical style: “Bookings are 1.5 times market cap! Wow! Absurd generational wealth opportunity! Everyone’s missing it! I can divide two numbers, look how impressive my investment judgement!”.