3 core ideas and 5 subtle insights from Value Investing: From Graham to Buffett and Beyond

The book delivers what it promises: a comprehensive and practical review of value investing. It is worth reading, even if you practice another framework. I work in expectations investing paradigm and Greenwald’s method gives me useful additional lenses. You can see how they work side-by-side in my free valuation tool based on SEC filings.

Modern value investing in a nutshell

1. Value of assets

Value investors in the 20th century searched for companies with market cap lower than net asset value (assets minus liabilities). It is unlikely that this approach will work well now because such obvious opportunities quickly become noticed and eliminated. But paying close attention to the balance sheet still very important because it is one of the most reliable sources of information we have on a company.

To get a useful estimate we shouldn’t stop with book value reported in 10-K. We need adjustments to reflect the economic reality of liquidation or reproduction of the business to reach the same level of revenue, for example:

We can use book value for cash and marketable securities, but other assets usually need adjustments1.

Not all assets appear on the balance sheet (for example, trained workers, customer relationships, product portfolio), but since a new entrant can't avoid spending on them to replicate the business, we should put a price tag here too.

Theoretically, long-term liabilities could be discounted by the cost of capital, but the effect is usually small (except for high inflationary environments).

2. Earnings Power Value (EPV)

By current earnings power we mean the average distributable earnings of a company as it exists today. This level of earnings is assumed to be constant over an indefinite future. The value of such a stream, the EPV, is calculated as this current earnings power divided by the company’s cost of capital. The cost of capital, in turn, is the expected annual return that the company must offer in order to attract willing investors.

The authors specifically stress that they don’t try to forecast future cash flows; the analysis should focus on sustainable earnings which exist today.

The most common approach to calculating EPV is to apply average margin level across different business cycles to the current year’s revenue2.

It is extremely important to make economically sound adjustments for accounting distortions, such as the difference between real and formal depreciation; using EBITDA is a dangerous shortcut.

3. Growth (maybe)

Growth doesn't necessarily create value. Growth always requires investment3, so it creates value only if these investments yield returns higher than the cost of capital. This idea doesn’t strictly belong to the value tradition; a DCF scenario with ROIC lower than WACC will paint a grim picture.

What characterizes Greenwald’s approach is extreme caution about growth. He doesn’t treat growth like any other knob in the model; he explicitly warns that only firms with moats — sustainable competitive advantages — can benefit from growth. Moreover, not every advantage is a real moat:

Deep pockets are not a moat: the company’s competitors are also large firms with equally large pockets.

A strong brand is not a moat, it is an asset whose value is equal to its reproduction cost.

Being a first mover is not a moat: history shows that pioneers often give way to competitive markets and don’t hold a dominant position for long.

Additional insights worth internalizing

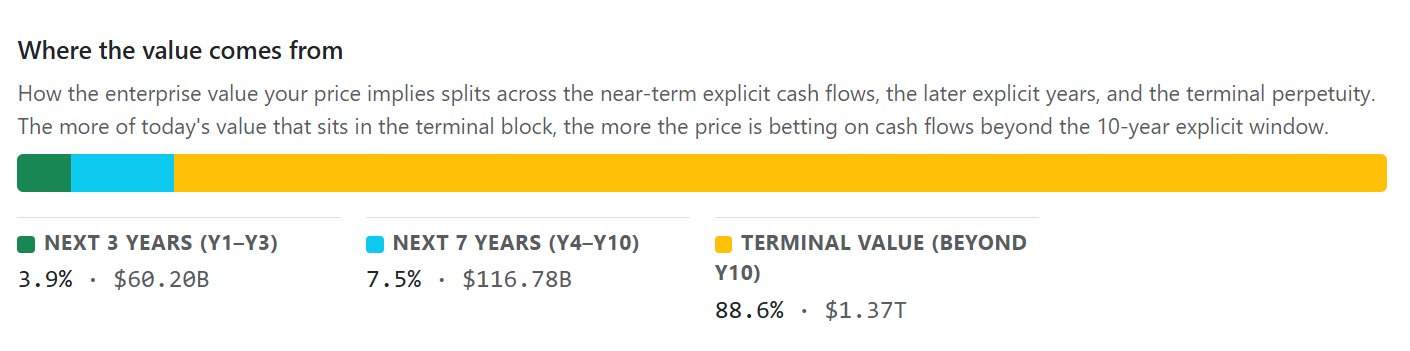

1. Mixing reliable and unreliable information in DCF analysis

Once the time value of money has been taken into account by the discounting process, all those individual cash flows are given equal weight. However, the near-term cash flows are measured with far more precision than those in the distant future. By weighting all cash flow present values equally, the NPV takes very good information—the near-term cash flow estimates—and adds it to very poor information—the distant future cash flow present value estimates. As any engineer will attest, the inclusion of bad information corrupts the whole. Large estimation errors in the bad information completely overwhelm the small estimation errors in the good information.

That is a sharp observation. Of course, when you do a DCF valuation, you are aware that the future might be materially different. But instead of shrugging it off as “it comes with the territory” we can at least roughly quantify how much of our present value comes from the near future, the more distant future, and terminal value.

I don’t see this split as a deciding factor on its own; but it helps to compare theses on different stocks. All other things being equal, I’ll pick the stock which gets more value coming from the next 3 years. So I made an addition to my expectations investing calculator:

2. Cost of equity estimation with venture capital as the upper bound

Venture capital firms report the levels of returns on their past funds and they respond to industry surveys asking directly for the level of expected returns necessary to market their latest venture funds. Not surprisingly, these figures tend to cluster together. Historically, these venture costs of capital have been as high as 18 to 20%. More recently they have been in the range of 13 to 14% as overall investment returns have fallen with interest rates. Required equity returns for established firms without dangerous levels of leverage should be below this venture capital level, at around 13% or less.

This approach provides a grounded sanity check on academic beta-based cost of equity calculations.

3. Dominant position on a small market as a moat: WD-40 example

Suppose an entrant could be economically viable at 30% market share and that the entrant would capture 0.5% market share per year, an optimistic figure for a product like WD-40 with a low price, low purchase frequency, and high search cost. Reaching a 30% market share would take 60 years. A 60-year path to economic viability would likely deter any rational potential entrant and bankrupt any irrational one. The strength of WD-40’s economic franchise depended paradoxically on the small size of its market. Remember the best defended monopoly is a single store in a town too small to allow for a second one.

4. No moat lasts forever; we should explicitly account for franchise fade

One way to start is by thinking of the half-life of the business, the number of years in the future at which its survival probability declines to 50%. For a durable franchise such as Coca-Cola, this might be 80 years or more. For a more recent tech dependent franchise such as Apple or Intel, it might be as brief as 15 or 20 years. The half-life can be translated into annual fade probabilities using the rule of 72. An 80-year half-life corresponds to an annual fade rate of roughly 0.9% (72 divided by 80) which will usually be immaterial (i.e., equivalent to an annual downward adjustment of 1% in the organic growth rate of value). But an 18-year half-life corresponds to a 4% fade rate (72/18), which is far more serious. In general, half-lives of 25 years or less, meaning at least 3% a year, need to be taken seriously. These annual fade rates (or extinction rates) are negative annual returns and must be covered by the margin of safety calculated without fade.

5. Catalysts doesn’t matter if a company have good management

There is a persistent belief among some value investors that unless there is an imminent catalyst that will drive market price to intrinsic value, then the value constituting the margin of safety will be “trapped” and never be realized. These are investors who never invest without catalysts. For them identifying and investigating catalysts is a central part of their research process. Given the Graham and Dodd analysis above, this outlook is misguided. For investments in companies that are well-managed, value does not get “trapped” even if the movement of price to full value takes a long time. True “value traps” are inextricably linked to poor managements. In that case, given the ability of bad managers to destroy value, it is a mistake to invest unless there is a clear, near-term prospect of management change. Otherwise, focusing heavily on catalysts is a distraction from other more important research areas.

On one hand, the logic is sound: good management of an underpriced firm will return money to shareholders via dividends and buybacks. But if a catalyst shortens waiting time for value to be recognized, it means better rate of return. A 50% appreciation in two months versus two years is quite different. My take: the difference between intrinsic value and market price of course is the main thing, but a catalyst on the horizon is definitely nice to have.

Those aren't all the insights the book has. I made a hundred notes on my Kindle, and learned a lot. So this book is an easy recommendation for any investor interested in individual stocks.

This publication is for informational and educational purposes only. It is not investment advice, tax advice, or a recommendation to buy or sell any security. I am not a licensed financial advisor. Investing involves risks, including the possible loss of capital. Always do your own research or consult a professional before making financial decisions.

The adjustments are usually not so important for current assets, but are critical and complicated for property and equipment. Here, we should take into account the discrepancy between real and accounting depreciation, inflation, technological changes that make new equipment more efficient, and so on.

This approach doesn’t work for highly cyclical businesses.

Even in the case of organic growth, a company must increase at least its working capital.