Why I bought Lululemon Athletica ($LULU) at $125

Reverse-DCF shows the market is pricing in a margin decline below the worst year in LULU's history. I'd take that bet.

LULU 0.00%↑ surfaced on my screener after another price drop this week. Mechanical valuation seems quite attractive.

Of course, relying on programmatic models is very risky, it’s just a starting point which requires careful adjustments and judgment calls1. What motivated me to dig deeper is the fact that part of the valuation compression seems to be about the narrative, like CEO controversy2, not about fundamentals.

Reverse-DCF of Lululemon: what does the price imply?

I am a big fan of the expectations investing framework: instead of projecting 10 years of cash flows, which is impossible by definition, we are just looking at a 10-year path which justifies the current price. The degree of plausibility of this path tells a lot about whether the company is fairly priced.

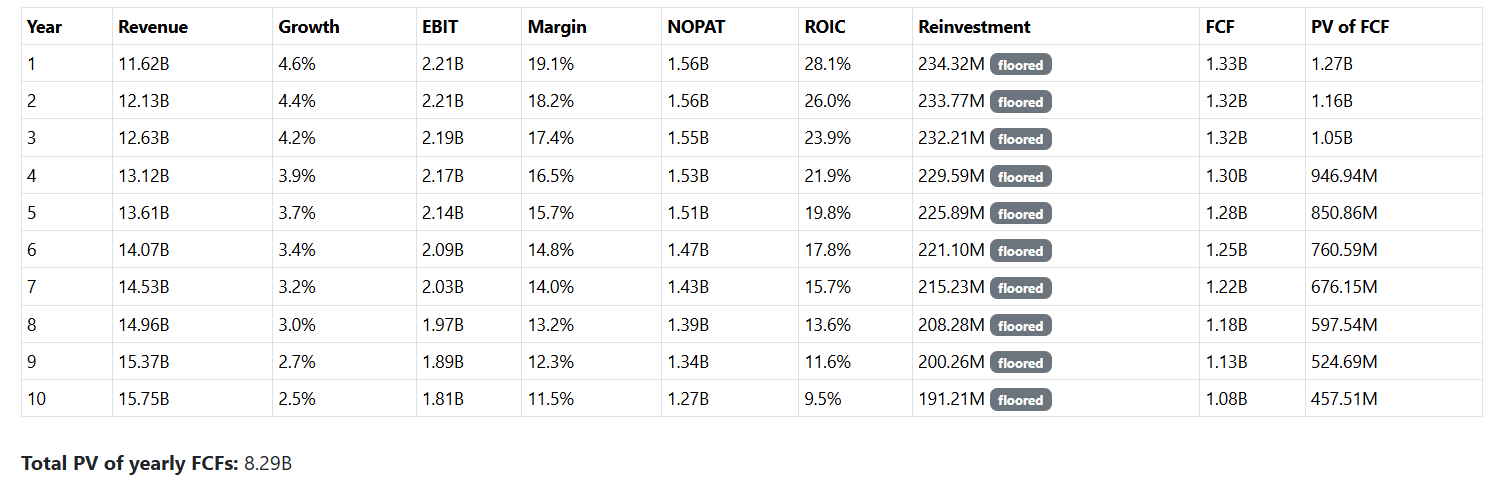

Here is one of the scenarios3 which fits the $125 price and 14.15B enterprise value:

You can see the full results and customize the output on the calculator page.

So what do we see here?

To justify the price the company needs to demonstrate a very moderate growth, gradually fading to the terminal 2.5%. The model allows both ROIC and EBIT margin to deteriorate quite significantly: from 28% to 9.5% and from 19% to 11.5%. Moreover, that’s under not-so-friendly other conditions: WACC 9.5% and minimum reinvestment 15% of NOPAT. If we ease WACC to 9% and reinvestment to 10%, the implied year-10 EBIT margin falls to 10%.

That doesn’t look like being priced for perfection. If all of them: low growth, sinking margins and falling ROIC are already baked in the price, there indeed might be an investment opportunity. It’s still too early to say that there is this opportunity. We need to assess the probabilities of different scenarios first.

Base case

Story: the business continues roughly on the current trajectory. Management doesn’t do anything revolutionary, but keeps financial discipline and executes the current strategy: more products in different categories. It means growing revenue but deteriorating margin (a wide selection of products competing with different brands naturally have lower margin than one iconic product). Growth in China and rest of the world continue to offset the decline in North America for several years.

Model assumptions: WACC 9%, terminal margin 14%, 5 years of growth on the last year pace, minimum 12% reinvestment.

Result: $18.09B enterprise value, $160 share price.

Bull case

Story: the business partially mitigates the brand’s struggle and tariffs effects. Several moderately successful products in the new categories without too much CAPEX for new locations. North American margins are flat and improving in China. In 10 years margin still deteriorates, but only to the point of observed historical minimum.

Model assumptions: WACC 9%, terminal margin 16.4%, several years of high single-digit growth, minimum 10% reinvestment.

Result: $21.47B enterprise value, $191 share price.

Bear case

Story: the business can’t sustain growth, pricing power declines. Despite high CAPEX spending, growth is only on terminal rate. China growth slows, so the offsetting effect on NA sales mostly vanishes.

Model assumptions: WACC 9.5%, terminal growth only starting now, 15% reinvestment floor, margin falls to 10%.

Result: $12.26B enterprise value, $108 share price.

Probabilities

That’s the hardest and the most interesting part.

First, about the bear case. It implies that several things happen simultaneously:

New products don’t bring growth.

China growth slows significantly.

All mitigation efforts on tariffs fail.

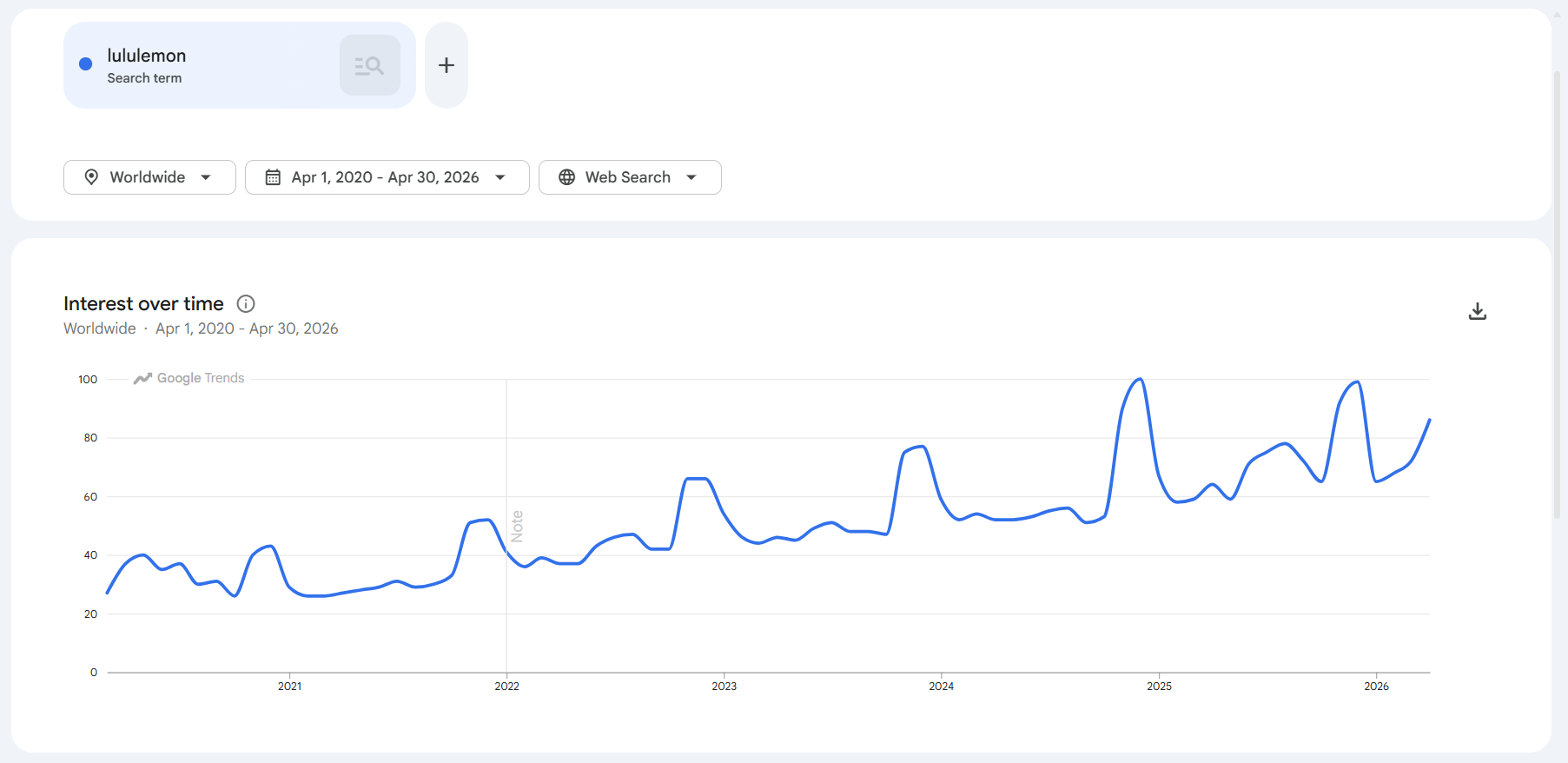

It doesn’t seem to be the case. Worldwide the brand shows growth after relatively weak December and January:

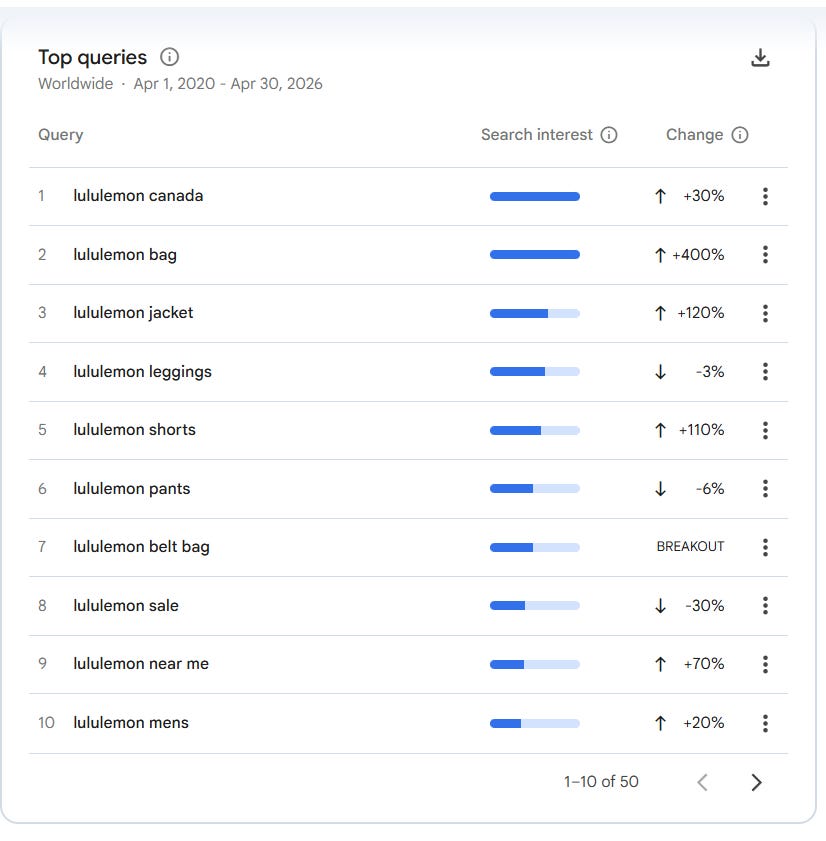

The new products demonstrate growing demand, while the iconic leggings decline:

That might indicate that the current strategy is actually correct: the demand for leggings would decline no matter what the company would do. It’s quite hard to milk one successful product indefinitely. So expanding into different product categories might be actually a solid, while less cool choice.

Anyway, I see no indication that all three things are here. At least growth is happening (though Q1 is likely to be weak). So the probability of the bear case looks relatively low. I assign 20%.

What we saw above is more consistent with the base case. I think 45% probability is appropriate here.

The bull case requires either tariff mitigation and flat North America sales, or stronger growth in China, or successful defense of margins. So there are several catalysts, each can give the market more optimism; they don’t have to happen simultaneously. That’s why I think bull case is more probable than bear. I assign 35% of probability.

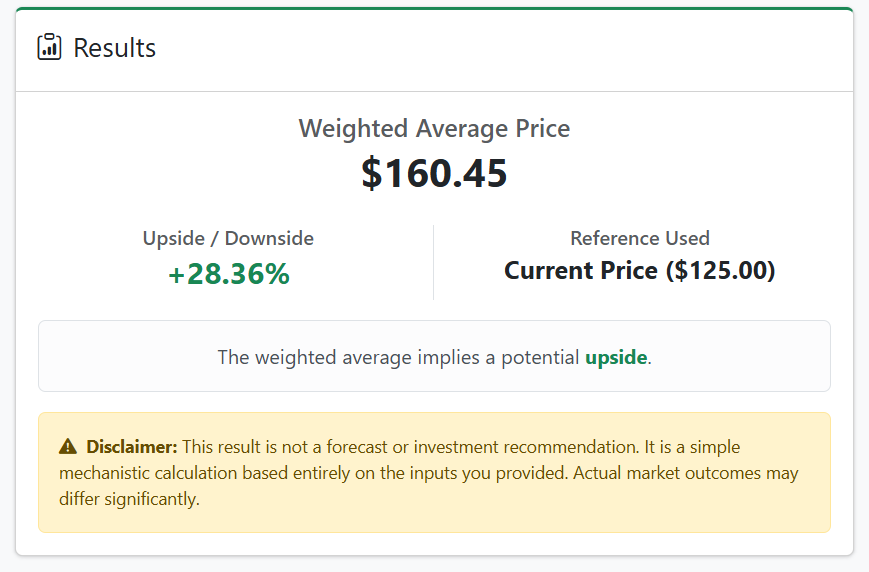

So what are we getting after weighing the probabilities and the prices:

The potential upside satisfies my personal margin of safety requirement. So I bought at $125 yesterday (12.05.2026).

Please note that it’s neither a buy recommendation nor a forecast. I am just sharing my own investment process. LULU fits my investment horizon and risk appetite. Quite possible it doesn’t suit yours. Do your own research.

It is not a generic disclaimer. Investing in LULU at this stage means bearing significant risks.

What can go wrong?

First, a meaningful turnaround is unlikely till the end of 2027. The new CEO starts in September; she simply has no time to make significant changes in 2026. The activist fight will continue to spoil the narrative, there is no clear deadline to end it. The further repricing catalysts in the future, the higher the risk that they will not materialize at all.

While the bear case scenario is relatively mild (just $108 vs $125) it doesn’t mean at all that price can’t go any lower. $108 is derived from a smooth 10-year path. If margin drops to 15% next year, the market will immediately react with a severe sell-off.

I might understate the risks of margin decline. If mentioned above drop to 15% margin materializes not as a one-time hit, but a new reality (for example in case of quicker decline of the leggings popularity), then path to 10% margin becomes much shorter and the real bear case would be around $80. I didn’t model it in the DCF because now I don’t see concrete indications for this scenario for now.

In case of constantly deteriorated narrative (“apparel brand for millennials, which lost its relevance”) the market can just suppress multiples and even if the math is correct, the shareholders will wait ~10 years while FCF gives the appropriate return.

I already mentioned that Q1 is likely still weak. There is no strong indicator that margins are holding. Judging by Google Trends, February and March were quite soft. If the next quarterly report shows EPS miss and weak margins, the price can easily drop below $100. If it happens, I intend to add to my position, provided the fundamentals still imply today’s long-term picture.

Conclusion

I see LULU as temporarily undervalued because of the combination of:

Negative publicity and CEO controversy.

Natural deterioration of the iconic product’s popularity.

Transition to multi-category strategy which is generally a good decision, but hasn’t yet yielded solid results.

Tariffs hit.

I don’t see them as company-destroying problems. I believe that lululemon athletica becomes more mature, diversified, less “cool” company, which can still create a lot of value for long-term shareholders. I also like their buyback program4. Not only because it mechanically supports price, but because it forces management to be more disciplined in capital allocation. Another healthy sign of a maturing company.

In short: LULU is not an “obvious buy”. It’s a messy, out of favor stock. That’s why there is a possibility of asymmetric returns: they come with risk.

Read next:

An update on Lululemon Athletica ($LULU) after the Q1 2026 report and new guidance

In May I initiated a LULU position at $125. Last week the company submitted a 10-Q report and issued guidance for 2026. The stock immediately dropped 10% and partially recovered in the following days; now it trades around $117. Many analysts downgraded their price targets.

This publication is for informational and educational purposes only. It is not investment advice, tax advice, or a recommendation to buy or sell any security. I am not a licensed financial advisor. Investing involves risks, including the possible loss of capital. Always do your own research or consult a professional before making financial decisions.

I recently shared a note with an example where mechanical models look stellar, but the actual investment thesis is weak. Always do you own research, no matter how convincing a thesis looks like.

There is a great article on Substack by Camille Moore: Lululemon Just Commited Brand Harakiri. I agree with the author about risks for the brand; but 12% price drop looks like overreaction. Plus, I think that the comment from Rodolfo Paiz:

What are the odds that the new CEO actually LEARNED from the experience at Nike and, having made all the mistakes (or seen her team make them, if you want to be generous), is now highly prepared to fix those issues at Lululemon?

might be on point.

Here are the inputs and assumptions I use in the model. Most of the numbers are from 10-K.

Diluted shares: 110,563,457 (adjusted with Treasury Stock Method); the effect on LULU is small, but I prefer to do it anyway. Full calculations: https://tools.theinvestlog.com/calculators/adjusted-shares/#LULU UPDATE 09.06.2026: the stated number is incorrect, it does not include exchangeable shares. Read the article with the updated model.

Total debt: 1798441000 (Non-current lease liabilities 1499717000 + Current lease liabilities 298724000).

Cash and equivalents: 1585150000 (Cash and cash equivalents 1807202000; applying 2% of revenue heuristic as a necessary maintenance CAPEX we are getting: 11102600000*0.02 = 222052000, so the adjusted cash is 1807202000 - 222052000).

Total stockholders' equity: 4961840000.

This year revenue: 11102600000, previous year revenue: 10588126000.

Annual operating income: 2210615000.

Effective tax rate: 29.47.

WACC: 9.5%. 0.5% higher than mechanical model produced because it uses β for the last 5 years, more recent data gives higher beta. Probably a bit higher than real though even considering LULU is 90% equity-financed.

Minimum reinvestment: 15% of NOPAT. Matches 3-year mean, which includes the phase with opening plenty of new locations. Probably a bit aggressive looking forward.

Terminal growth rate: 2.5%.

10-K:

Over the course of 2025, we repurchased 5.0 million shares for $1.2 billion, and in December 2025, our board of directors approved a $1.0 billion increase to our stock repurchase authorization.